NAND Flash Prices Are Surging in 2026 — What It Means for Your Supply Chain and How to Prepare

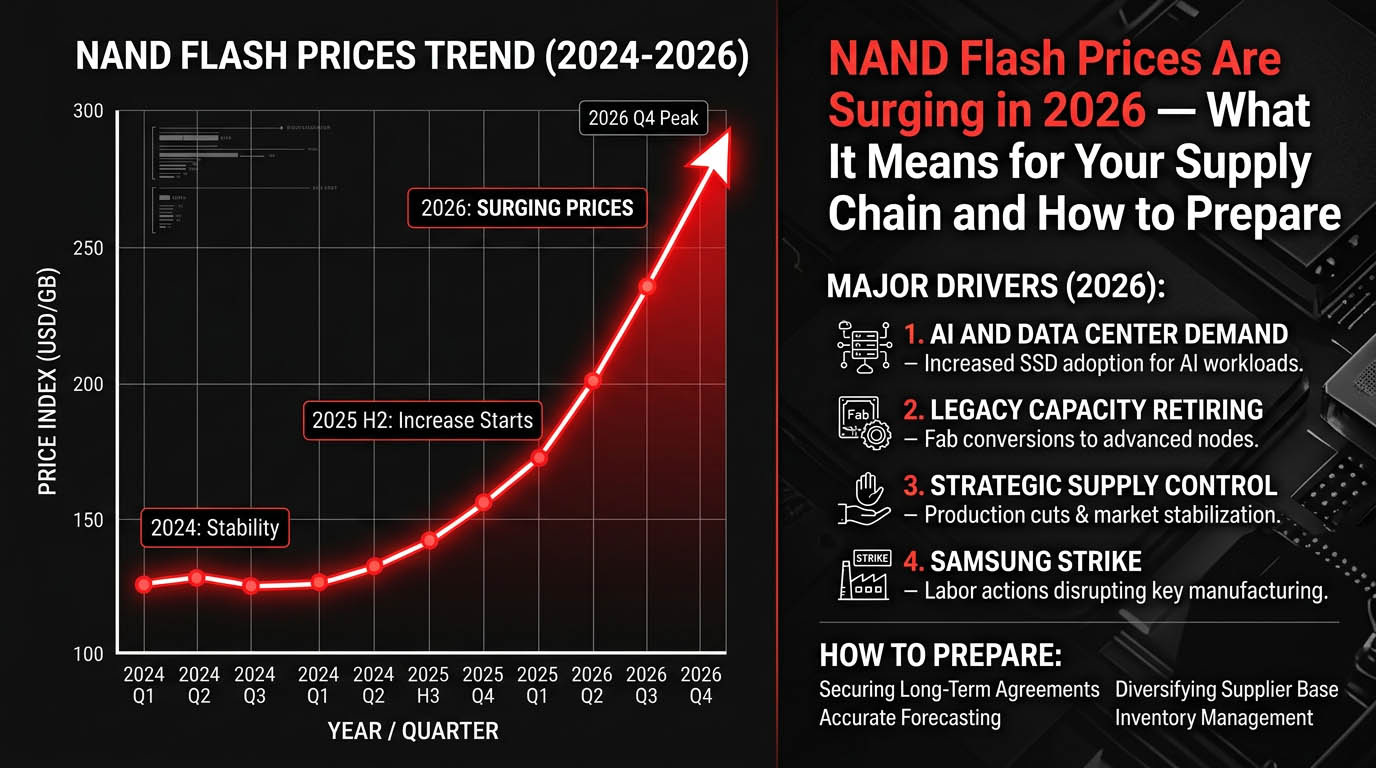

If you ordered NAND flash memory in January, you thought the 33% price jump was a one-time shock. It was not.

TrendForce now projects Q2 2026 NAND Flash contract prices will rise another 70% to 75% quarter over quarter. That comes on top of a 33% to 38% increase in Q1. Samsung, SK Hynix, and Micron have launched a second wave of coordinated price hikes starting in April, and this time there is no sign of a quick reversal.

For a photographer who just needs a 128GB SD card for a weekend shoot, this means paying 50% more at Best Buy. For a procurement manager buying 50,000 microSD units for a consumer electronics line, it means rewriting the entire cost model. And for the foundries making these chips, it means finally recovering from years of margin compression — at the cost of strained customer relationships.

This is not a short-term fluctuation. It is a structural supply crunch. Every buyer, from enterprise SSD manufacturers to SD card brands, needs a plan.

The Numbers: A Price Surge Without Precedent

To understand where we are, it helps to trace the timeline.

November 2025. NAND wafer contract prices for certain categories jumped over 60% in a single month. The industry shrugged it off as a seasonal anomaly — year-end inventory adjustment, nothing to worry about.

January 2026. NAND Flash contract prices surged approximately 65% month over month, setting a record high. Suppliers began warning customers about allocation limits. The "temporary" narrative started to crack.

Q1 2026. Product-level prices — the numbers that actually matter to SSD makers, memory card brands, and device OEMs — climbed 33% to 38%. The pain finally reached downstream buyers. Procurement teams started receiving revised quotes weekly instead of quarterly.

Q2 2026. Contract prices are expected to rise another 70% to 75%, according to TrendForce and reports from Bonpain and 199IT (April 26, 2026). This is the number that has supply chain managers rewriting their forecasts.

For context, DRAM is feeling similar pressure: Q1 rose 55% to 60%, and Q2 is projected to climb 58% to 63%. The entire memory market is tightening simultaneously, which means there is no easy substitution between memory types to relieve the squeeze.

The global NAND Flash market is estimated to reach $65 billion in 2026 and $70 billion in 2027. The revenue growth looks impressive on paper, but the capacity to serve this demand is not expanding fast enough. Revenue growth driven by price increases is not the same as healthy market growth.

Why Prices Are Rising — Five Converging Forces

This surge does not have a single cause. Five forces are pushing in the same direction, and none of them will reverse quickly.

1. AI and Data Center Demand

Enterprise SSDs and AI servers are consuming NAND at a rate the industry has never seen. Training clusters, inference workloads, vector databases, and high-performance storage arrays require massive amounts of high-density flash. A single AI training cluster can consume as much enterprise SSD capacity as thousands of consumer laptops.

Every wafer allocated to enterprise products is one fewer wafer available for consumer-grade storage — the SD cards, microSD cards, and USB drives that millions of people rely on daily. The math is simple and brutal: when AI pays premium prices, consumer products get rationed.

2. Foundries Pivot to HBM

Samsung, SK Hynix, and Micron are redirecting their most advanced fabrication capacity toward HBM — High Bandwidth Memory, the critical component for AI accelerators. SK Hynix signed a landmark "Stargate" cooperation agreement with OpenAI, signaling how deeply memory supply is now entangled with the AI infrastructure buildout.

HBM commands significantly higher per-wafer margins than standard NAND. For a foundry that has spent two years watching margins compress, the economic incentive to shift capacity is irresistible. The result is predictable: NAND production gets squeezed, even as total wafer starts remain flat or grow modestly.

3. Legacy Capacity Retiring

Older process nodes — the ones that produce cost-effective 512GB TLC and similar density chips — are being phased out. Fabrication equipment is reaching end of life, and foundries are not reinvesting in mature-node capacity when cutting-edge nodes offer better returns.

Products that depend on these legacy densities are hit hardest. Many SD cards, mid-range SSDs, and embedded storage solutions still rely on 512GB TLC and similar specifications. When the fabs that make these chips close, the supply does not just shrink — it disappears.

4. Strategic Supply Control

Several suppliers have paused their 2026 quotations entirely, waiting for capacity allocation clarity before committing to prices. This is a rational business decision — nobody wants to sell at today's price when tomorrow's price might be 30% higher. But from the buyer's perspective, it feels like being locked out of the market.

The withholding of supply creates artificial scarcity that compounds the genuine shortage. It is a game of chicken between foundries and buyers, and the foundries hold all the cards.

5. End-Market Recovery

Smartphone, PC, and automotive markets are all recovering simultaneously. Each sector is building inventory to hedge against future shortages, which pulls even more demand into an already tight market. The automotive sector deserves special attention: modern vehicles carry 100GB or more of flash storage for infotainment, ADAS, and telemetry systems. As electric vehicle production scales, automotive NAND demand grows structurally, not cyclically.

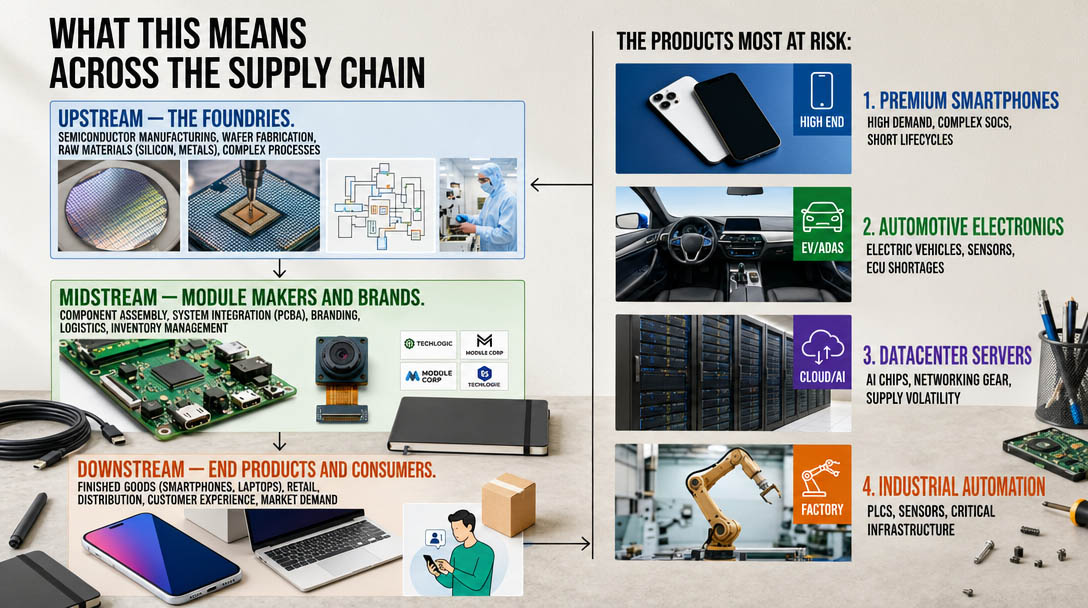

What This Means Across the Supply Chain

The pressure is not distributed evenly. Here is how it breaks down at each level.

Upstream — the foundries. Samsung, SK Hynix, Micron, and Kioxia are seeing revenue improvement after a brutal downturn cycle. But they face intense internal pressure to allocate capacity between HBM, which offers premium margins, and standard NAND, which drives volume. Samsung's recent labor strikes add another layer of uncertainty to their production schedule. For the foundries, this is a golden moment — but one that risks long-term customer relationships if the pain gets pushed too far downstream.

Midstream — module makers and brands. The squeeze is real and public. SanDisk has announced double-digit price increases across all channels. Kingston has issued supply warnings, predicting that shortages will intensify through the second half of 2026. For SD card and memory card manufacturers, raw material costs are climbing at a rate that cannot be fully absorbed internally. The question every brand faces is the same: how much cost to pass on to customers, and how much to eat in order to maintain market position?

Most brands are choosing a middle path: phased increases with advance notice, combined with product portfolio adjustments that steer customers toward higher-margin SKUs.

Downstream — end products and consumers. Every device with flash storage is affected: smartphones, laptops, automotive systems, gaming consoles, security cameras, drones, and industrial equipment. The cost pressure ultimately flows to the consumer, but not immediately. Brands are trying to delay price passthrough as long as possible to maintain market share.

For the average consumer, the impact shows up in three ways: higher prices for memory cards and USB drives, fewer promotional discounts on storage products, and in some cases, products simply going out of stock. The era of "just buy an extra 256GB card for $20" is pausing.

The products most at risk: Micro SD cards, SD cards, CFexpress cards, USB flash drives, and consumer SSDs. These products compete for the same NAND pool as higher-margin enterprise products, and they are losing that competition.

Market Outlook: When Does It Ease?

The short answer: not in the next two quarters.

Supply tightness is expected to persist through the second half of 2026. AI-related demand will continue to grow as a share of total NAND consumption, and foundries have no incentive to redirect capacity away from HBM toward standard NAND. The capacity gap between supply and demand is projected to widen before it narrows.

One factor that could reshape the market: Chinese domestic foundries, particularly YMTC (Yangtze Memory Technologies), are expanding their Xtacking-based NAND production. If they can ramp capacity quickly and compete on price, they may provide an alternative supply channel for cost-sensitive buyers. YMTC has already demonstrated competitive technology at 232-layer and beyond. However, geopolitical factors, export controls, and qualification timelines add significant uncertainty to this path.

The global market will reach $65 billion in 2026 and $70 billion in 2027. Growth is strong, but growth does not mean availability. Companies that plan for scarcity will survive this cycle. Companies that wait for prices to normalize will not.

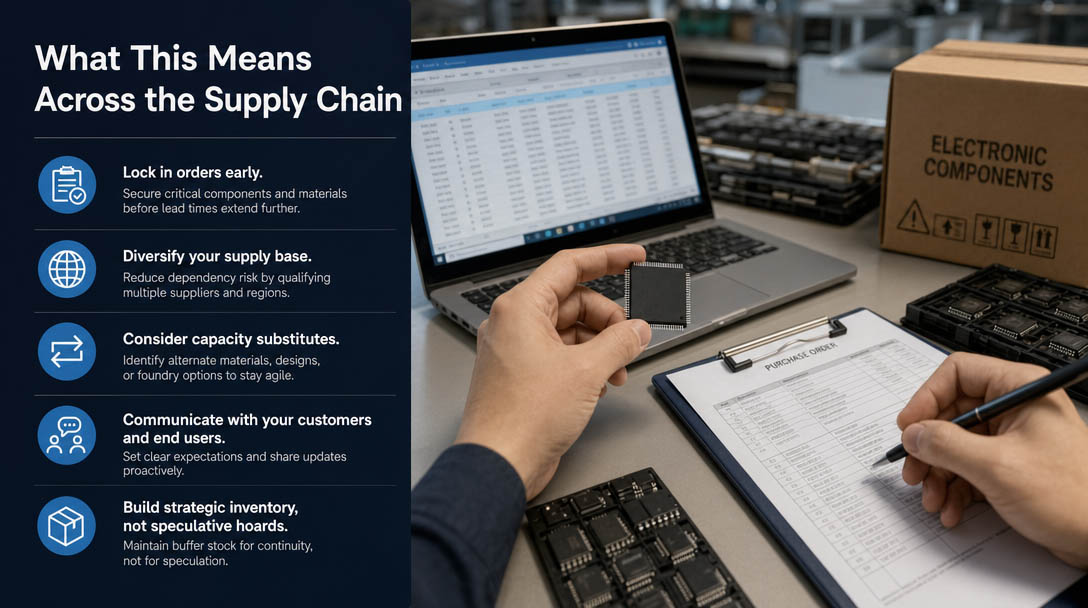

What Buyers Should Do Now

If you procure NAND-based products — whether you are a wholesale distributor, an OEM, a system integrator, or a brand owner — waiting is the most expensive strategy available. Here is a practical action plan.

Lock in orders early. Spot prices will continue to climb. Forward commitments at current rates are almost certainly cheaper than anything available in Q3 or Q4. If your supplier offers quarterly or semi-annual pricing agreements, take them now. The cost of being wrong (prices drop slightly) is far less than the cost of being right (prices continue rising and you have no supply).

Diversify your supply base. Relying on a single brand or a single distribution channel is a risk you cannot afford right now. Evaluate alternative manufacturers and secondary suppliers who may have allocation agreements that give them priority access. A second source at a slightly higher price is better than no source at any price.

Consider capacity substitutes. If 512GB TLC is unavailable or overpriced, can your product specifications shift to 256GB or 1TB SKUs? In some cases, re-engineering your bill of materials to use a different density, interface, or even a different memory technology (such as combining NAND with NOR for specific use cases) can save significant cost and improve supply security.

Communicate with your customers and end users. Transparent communication about pricing timelines helps downstream buyers plan their own purchases. A proactive message in May is infinitely more valuable — and better received — than a surprise invoice in August. For B2C brands, this means updating retail pricing strategies and preparing customer communications that explain the market dynamics without creating panic.

Build strategic inventory, not speculative hoards. There is a difference between maintaining a responsible safety stock and gambling on further price increases. Plan for your actual 6-to-9-month demand, not for a hypothetical price spike that may or may not materialize. Storage costs and capital tie-up are real constraints.

How Hugdiy and MRT3C Are Responding

As a memory card manufacturer with direct supply chain relationships, Hugdiy (hugdiy.com) and its MRT3C brand are committed to maintaining production continuity through this disruption. We are securing allocation through multi-quarter agreements with upstream partners, and we are prioritizing fulfillment for existing B2B partners who have standing orders.

We understand that our customers face their own pricing pressure from their end users. Our approach is not to maximize margins during a shortage — it is to maintain a sustainable partnership that survives the cycle. That means:

- Volume quotation with locked-in pricing windows so you can plan your own costs

- Capacity planning transparency — we will tell you honestly what is available, what is constrained, and what the timeline looks like

- Product alternatives — if your preferred specification is unavailable, we will suggest functional equivalents that meet your performance requirements

- No surprise allocations — if we commit to a delivery, we deliver

For B2B buyers who need reliable supply and honest communication during a market that rewards neither, that matters.

Contact us for the latest pricing and supply plan. The market will not wait, but preparation buys you options.

*Data sources: hugdiy.com, MRT3C,TrendForce , Morgan Stanley, Bonpain , 199IT. All price projections are estimates as of April 26, 2026 and subject to market changes.*